Why is Investment Due Diligence Necessary?

Due diligence is the detailed investigation that a potential investor carries out on a target business after successfully completing preliminary negotiations with its owner.

Notwithstanding, the differences in scope due to different investing scenarios, there are typically four types of due diligence. These include commercial, legal, financial, and tax checks.

As a result of the due diligence, the investor may come to a different or more nuanced understanding of the opportunity and seek to renegotiate the initially agreed terms or even decide to decline the investment.

Due diligence commonly results in the investor negotiating additional, more detailed terms and conditions in its final agreement with the business's owner.

Notwithstanding, the differences in scope due to different investing scenarios, there are typically four types of due diligence. These include commercial, legal, financial, and tax checks.

As a result of the due diligence, the investor may come to a different or more nuanced understanding of the opportunity and seek to renegotiate the initially agreed terms or even decide to decline the investment.

Due diligence commonly results in the investor negotiating additional, more detailed terms and conditions in its final agreement with the business's owner.

What are the Steps Required for Investment Due Diligence?

Due diligence begins after an investment has been initiated via a letter of intent, or term sheet. At this point, a team is assembled to conduct the exercise with relevant rules of engagement agreed between both parties.

Investment due diligence is usually taken over a period of between 30 and 60 days.

In the end, a report will be compiled and presented to the investor with recommendations of potential additional terms and conditions to be required in the transaction.

Investment due diligence is usually taken over a period of between 30 and 60 days.

In the end, a report will be compiled and presented to the investor with recommendations of potential additional terms and conditions to be required in the transaction.

Types of Investment Due Diligence

Investment due diligence does not have a strict formulation; it should be designed to address the specific circumstances. The matters which will be investigated depend on the structure of the contemplated transaction - what the investor will receive in exchange for its investment. If the transaction is structured so that certain assets, liabilities or segments of the business are excluded, there usually is no reason for the investigation to cover them.

Due diligence will include commercial, legal, financial and tax due diligence

1. Commercial due diligence covers the target business’s market positioning and market share, including drivers and prospects. It seeks to obtain an independent perspective on the sales forecast as the most critical component of the target’s business plan.

2. Legal due diligence covers a wide scope of legal matters, including proper incorporation and ownership, contractual obligations, ownership of assets, compliance and litigation. It seeks to confirm the validity of the rights being acquired by the investor and the absence of legal risks which could undermine the value of the investment.

3. Financial due diligence has a wider perspective because it seeks to both:

- Validate the investor’s valuation assumptions by looking at historical performance, if available, and concluding whether it is consistent with projections, and

- Identify financial uncertainties and exposures which could disrupt the business, or result in additional costs to the investor.

4. Tax due diligence could be viewed as an extension of the financial due diligence, where the focus is on identifying potential additional tax liabilities arising from non-compliance or errors.

Further types of investment due diligence are technical, environmental and regulatory, performed when the impact of these areas on the business is significant. Depending on the situation, the due diligence may need to address very specific and narrowly defined topics, as long as they are factors for the valuation and assessment of the risks of the investment opportunity.

2. Legal due diligence covers a wide scope of legal matters, including proper incorporation and ownership, contractual obligations, ownership of assets, compliance and litigation. It seeks to confirm the validity of the rights being acquired by the investor and the absence of legal risks which could undermine the value of the investment.

3. Financial due diligence has a wider perspective because it seeks to both:

- Validate the investor’s valuation assumptions by looking at historical performance, if available, and concluding whether it is consistent with projections, and

- Identify financial uncertainties and exposures which could disrupt the business, or result in additional costs to the investor.

4. Tax due diligence could be viewed as an extension of the financial due diligence, where the focus is on identifying potential additional tax liabilities arising from non-compliance or errors.

Further types of investment due diligence are technical, environmental and regulatory, performed when the impact of these areas on the business is significant. Depending on the situation, the due diligence may need to address very specific and narrowly defined topics, as long as they are factors for the valuation and assessment of the risks of the investment opportunity.

How Does it Actually Work?

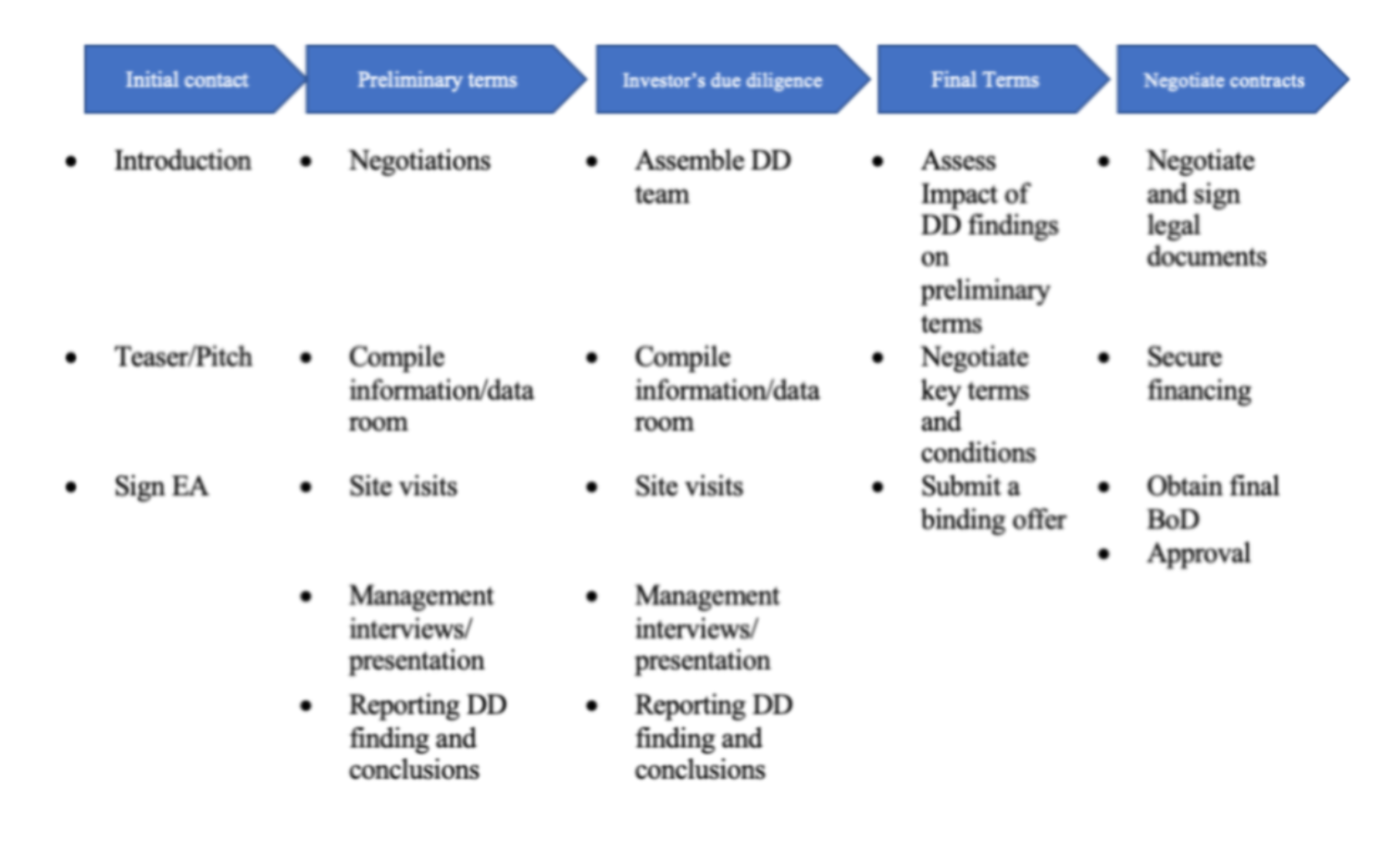

Investor due diligence typically takes a central position along the timeline of the investment process, as illustrated by the chart below

1. The potential investor has expressed its interest in the opportunity presented by the investee (founder, business owner, supplier, etc.).

2. The two sides have met and established a relationship, discussed the opportunity, and agreed in principle on the key terms of the investment (transaction).

3. The key terms agreed in the preliminary stage typically include transaction structure (what does the investor receive?), Price (what does the investor pay?) And process (what steps must be completed to close the transaction?). Frequently, such terms are laid out in a non-binding document called a Letter of Intent, Term Sheet or Memorandum of Understanding.

Process of Due Diligence

• The investor and the investee agree on the terms of access to information about the target business, including confidentiality undertakings, scope, and limitations of the investigation, communication protocol and points of contact.

• A timeline is established including deadlines for receiving the information, issuing the investment due diligence report (s) and returning to the negotiating table.

• Information requesting and receiving.

• Project / Site visits at the target business by the due diligence team.

• Internal communication and discussion of findings.

• Preparation of one or more investment due diligence reports.

• Discussion of the report with the investor.

• Our lawyers will put the investment due diligence findings on the table in order to negotiate the changes or additions to the terms of the transaction.

• A timeline is established including deadlines for receiving the information, issuing the investment due diligence report (s) and returning to the negotiating table.

• Information requesting and receiving.

• Project / Site visits at the target business by the due diligence team.

• Internal communication and discussion of findings.

• Preparation of one or more investment due diligence reports.

• Discussion of the report with the investor.

• Our lawyers will put the investment due diligence findings on the table in order to negotiate the changes or additions to the terms of the transaction.

Our Services

Due Diligence in Thailand

Protect your investment and gain peace of mind by using our due diligence service. Choose the level of review you believe suits your needs or contact us for assistance in making the right choice.

Commercial and Civil Litigation in Thailand

LITIGATION IS SORT OF A GAME. THERE IS A WINNER AND A LOSER. WE KNOW HOW TO WIN

Investment Disputes in Thailand

Juslaws and Consult have an extensive business litigation practice. Included are civil trials in state and federal courts, as well as appeals, mediation, and arbitration.

Business and Trade Disputes in Thailand

Juslaws lawyers are experts in claiming back lost investments and have has many years of practice in this field.

Property and Land Disputes in Thailand

We provide comprehensive legal services to foreign clients. All our lawyers and consultants are English speaking.

Criminal Court and Police Cases in Thailand

Juslaws & Consult has a specialized criminal litigation and our legal department capable of representing clients in Thailand with pending court cases and in arbitration.

Book a Free Consultation to Discuss Your Case in Thailand

Contact the team of Juslaws Litigation Lawyers today to schedule a free 1-hour consultation to review your case and available options.